First, let’s lay an overview of what an investment robo-advisor does. A robo-advisor refers to software that functions by providing online investment and financial management advice.

Robo-advisors need minimal human intervention as they use advanced mathematical algorithms. Accordingly, these algorithms serve this end by allocating, managing and optimizing a client’s assets.

I highly recommend you watch this great 4 minute video from The Wall Street Journal, which gives you a basic overview of what robo-investor companies do.

Robo-advisors came to the forefront around the time of the global financial crisis in 2008. This is because the investor’s confidence in the people pulling the strings of global finance was probably rattled. As a result, the option of independent robot advisors naturally seemed appealing.

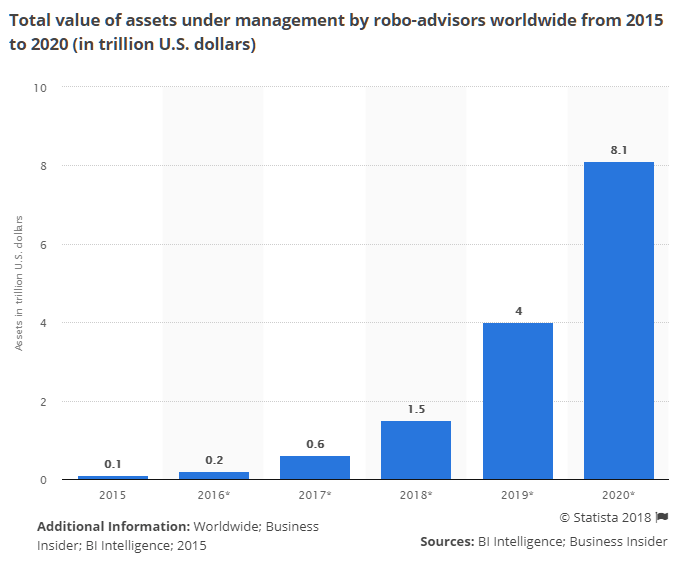

The robo-advisor market is growing rapidly, as more people learn about the benefits of using premier robo-advisors like Betterment and Wealthfront.

Now, armed with this understanding, let’s get to the focus of this article. Betterment and Wealthfront are two premier robo-advisors which offer excellent services. As such, a brief pointed analysis of the respective advisors can lead us to an informed and objective determination.

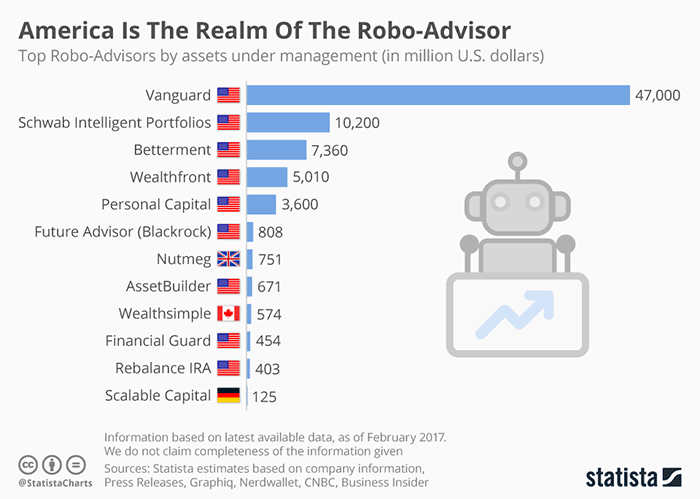

Betterment and Wealthfront rank #3 and #4 for most assets managed.

Betterment Overview

Betterment emerged in 2008 and is generally considered to be the pioneer robo-advisor. Unsurprisingly, this secured its position as the leading robo-advisor early on. As a matter of fact, it still boasts 300,000 clients and a staggering $13 billion in assets under management today.

The fundamental concept Betterment embodies is risk tolerance assessment. Betterment determines your risk tolerance and then creates a portfolio to place a user in an asset allocation of exchange-traded funds (ETFs) contingent on your tolerance.

If you are not familiar with ETFs, then take two minutes to watch this simple explanation video from Bloomberg Magazine, which explains what an ETF is.

Accordingly, Betterment gives fiduciary advice. Moreover, by virtue of being an independent advisor, the software has no funds of its own to push. This means that you can have peace of mind with the assurance that the information is objective and best for your investment portfolio.

Notably, the Modern Portfolio Theory (MPT) guides the investment process. This is important because proper asset allocation is the main focus, rather than individual security selection, which is not nearly as important.

There are two service options available; the Betterment Digital and Betterment Premium. The Betterment Digital service has no account minimum and has an annual charge of 0.25% on managed assets. The Premium option offers unlimited phone access to financial advisors at a 0.40% fee per annum. Notably, Betterment premium works for investors with a minimum of $100,000 in their account. Betterment has an offer of free management for one year for users who deposit more than $10,000.

Here’s a great interview with Betterment’s CEO, John Stein, where he breaks down why robo-investing is fast becoming the best way to wisely invest your money.

Wealthfront Overview

Wealthfront is another top-notch robo-advisor on the market. Interestingly, Wealthfront was previously named KaChing until 2011.The platform essentially emulates the portfolios of stock professionals with money instead. Wealthfront is now a significant force with assets under management amounting to $10.5 billion.

The platform operates by asking respective users a series of questions on sign-up and determines asset allocation based on these answers. These democratized services have propelled Wealthfront to the heights it enjoys currently.

The team behind this successful robo-advisor is led by renowned economist Burton Malkiel. He serves as the Chief Investment Officer for the site. Additionally, there are other world class financial experts to facilitate Wealthfront.

Here is a very informative interview with the founder of Wealthfront, Andy Rachleff, explaining exactly how their robo-advisor works in a nutshell.

Notably, there is a minimum deposit of $500 to open an account. Once a user deposits money into their Wealthfront account, they can pick between the taxable or tax deferred account options. Correspondingly, Wealthfront allocates a user’s investment into an array of ETFs. The Royal Bank of Canada holds funds for this platform.

Like Betterment, this robo-advisor relies on Modern Portfolio Theory to allocate assets automatically. This is contingent on a user’s risk tolerance and actual financial needs. Additionally, there is automatic rebalancing to ensure the allocation is done correctly. Wealthfront makes these determinations using questionnaires during the opening of a new account. The findings facilitate appropriate asset allocation and these determinations will remain regardless of amounts deposited.

Wealthfront also relies on the Path Savings Model, which can enable a user to set significant saving goals. These include retirement savings, college tuition for kids and even purchasing a house. Path is incorporated into Wealthfront systems and shows you, for lack of a better description, if you are on the right investment path. This is because Path generates scenarios based on analysis of all your accounts, and this is tabulated into meaningful savings advice.

There is also a service called SmartBeta for those with over $500,000 in holding. This is to maximize a user’s return from core market indexes.

Wealthfront does particularly well with taxable accounts and can minimize your annual tax expenses. This is a crucial design aspect as the entire point of a robo-advisor is optimum asset management.

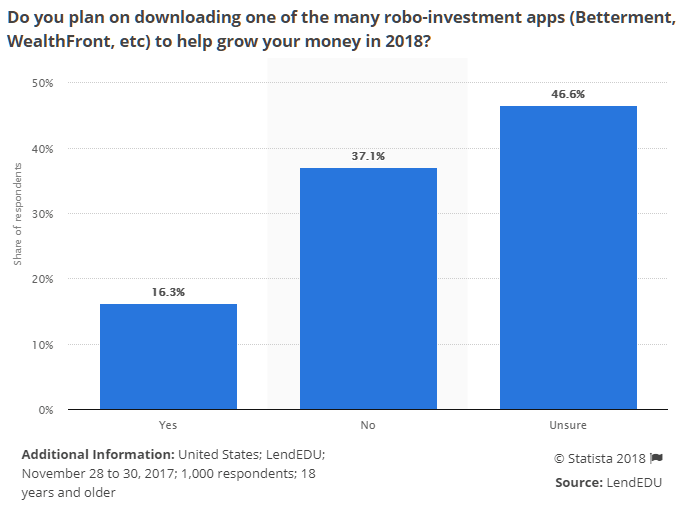

In 2018, over 16% of adults in the United States plan on using Betterment or Wealthfront.

Betterment Advantages (The Pros)

#1 Absence of Account Minimums

Had to go first, right? This is because among robo-advisors, the lack of a minimum deposit is a rarity. Notably though, this is not the case for the Betterment Premium which in turn offers greater access to financial advisors.

#2 The Modern Portfolio Theory

This investment philosophy brings along the benefits of diversification in investing. As a result, the company uses ETFs which denote up to 12 different asset classes. There is a social aspect to the portfolio as well. This is because investors get to choose companies whose business practices align with their preferred social values. Artificial Intelligence ETFs are crucial to this end, and they execute an exclusion process called negative screening. The positive companies in this light are vetted through a process called positive screening. There is also a ‘flexible portfolio’ tool for users who wish to tailor the amount of money invested, in particular ETFs. Notably, this is only available to users with over $100,000 in their account.

#3 Automatic Rebalancing

The investor portfolios are also rebalanced as needed. Automatic rebalancing happens every time cash flows in an out of the investor’s account. This is in the form of transactions like withdrawals and dividend payments. The company purchases fractional shares so that there is no uninvested cash in your portfolio. For Betterment Premium investors, there is the advantage of the account being monitored by designated financial advisors.

In the video below the CEO of Betterment tells The Wall Street Journal some of the details of the most important advantages of their service.

#4 Goal Based Saving

From the initial sign up process, the goal setting process begins. A user gives details like their age and annual income. The company then suggests a series of saving goals. The specific goals set come with recommended asset allocation and targets. The personalized goals therefore guide the asset allocation process and optimize investor earnings. Additionally, there is a Retire-Guide feature that allows you to link your non-Betterment accounts. This can help you get a better picture of your retirement and savings accounts. Retire-Guide compares the savings amounts in your accounts to your average spending amounts during retirement. This is crucial to help determine if your savings plan is sustainable or not. Accordingly, you can make the necessary adjustments to effect the same.

#5 Fair Management Fees

The 0.25% charge that Betterment Digital offers is quite affordable relative to most robo-advisors. Even the services of human advisors that Betterment offers as a fiduciary advisor are reasonable.

#6 SmartDeposit

This optional feature is yet another measure to optimize your resources. SmartDeposit harvests unneeded cash from your checking account and places it in productive use.

#7 Charitable Donations Options

Charitable donations can be a part of a successful investor’s portfolio. Accordingly, Betterment offers a tax-compliant channel to donate appreciated securities to charities. This means that the donations can be accountable and streamlined.

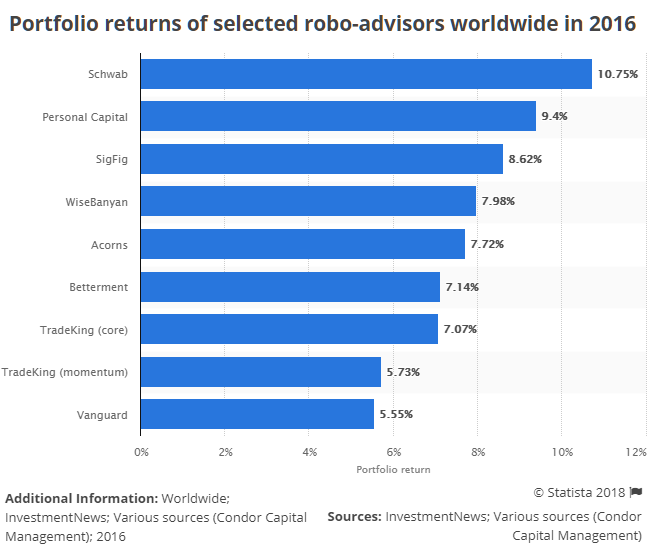

In 2016, Betterment’s average return and performance ranked number six in the world.

Betterment Disadvantages (The Cons)

Betterment has a whole lot of advantages. Still, there are some facets that can improve to make the great service even better. These include…

#1 Absence of Direct Indexing

Why is this relevant? Most robo-advisors have the tax loss harvesting mechanism to review investments daily and reduce tax exposure. A direct indexing tool like the one Wealthfront buys single securities on an index to isolate tax loss harvesting opportunities. As a result, investors with taxable accounts are guaranteed significant savings. This takes away the reliance on ETF tracking on the index, which is not as efficient.

#2 Safety Net Goals

Betterment has an investment strategy which entails 40% investment in stocks and 60% in bonds. This essentially involves investing emergency funds. However, the logic of safety net investments is questionable since it is a short term saving. You’ll need to decide if investing your emergency fund is really advisable. The capital gains tax implications are noteworthy since short-term capital gains are taxed higher.

If you still want to find out more about Betterment, then here is a great video review of Betterment.

Here is an actual Betterment customer, who discusses her experience and returns over a year and a half of using Betterment.

Wealthfront Advantages (The Pros)

#1 Account Minimums

For comparison’s sake it’s important to mention that Wealthfront has a minimum deposit of $500 USD to open an account. This is generally insignificant for most investors because the average portfolio is worth a lot more. The fees are fair with an annual fee of 0.25% for asset management. This fee is waived for the initial $5000 USD. This makes it one of the cheapest robo-advisors as the fees are inclusive of ETFs.

#2 Retirement Savings Plan Using the Path Strategy

The path algorithm is excellent in determining the efficacy of your retirement savings. The service is integrated into the Wealthfront interface. The user fills a questionnaire meant to assess spending habits. It is these spending habits balanced against your allocated savings during retirement that determine your retirement viability.

#3 Tailored Transfers

This is a feature exclusive to Wealthfront. Ordinarily, the process of moving from a different advisor or brokerage involves moving in cash. Instead, Wealthfront offers the option of asset transfer into a diversified portfolio over time. That said, Wealthfront contends that incompatible assets like stock options. The importance of the tailored transactions is the avoidance of tax bill duplicity.

#4 There is a Wealthfront Referral Program

This incentive means you get an additional $5,000 in assets or cash managed free for every customer referred to Wealthfront.

#5 Portfolio Review and External Accounts

This tool gives users the ability to pull in other accounts and centralize them. This enables a user to receive Wealthfront feedback on fees, taxes and related information.

#6 529 College Savings Plan

This is a great option to prioritize saving for your kid’s college fund. Accordingly, management of the first $5,000 is free. The college savings plan can show a user what options they have over and above their short-term goals. In this era of crippling student debts, the planning and execution of solid tuition plans is perfect.

#7 Portfolio Line of Credit- This is another feature exclusive to Wealthfront. The caveat is that the service is available for those taxable accounts with over $100,000. The investors who fit this bracket can take a line of credit against their investments for up to 30% of the value of their accounts.

Here is a tweet from Wealthfront’s CEO showing their returns and performance.

Since our inception 6 years ago @Wealthfront generated a 10.02% avg annual return (on a risk 8 portfolio) despite 4 market corrections. That does not include tax-loss harvesting benefit which could have added up to 2.25% annually depending on your tax rate https://t.co/WMEY9Vm3qA

— Andy Rachleff (@arachleff) February 16, 2018

Wealthfront Disadvantages (The Cons)

#1 Minimums

In the grand scheme of things, this is an unfortunate negligible detail. This is because the ordinary investor who relies on robo-advisors wouldn’t typically have a portfolio in the $500 range. Besides, Betterment Premium, which is the comparable service, is not free either. Therefore, this is a shortcoming that might make for a great tagline but has little practical implication. Betterment has a greater proportion of accounts than assets on Wealthfront. This may be attributed to this disparity.

#2 Absence of Fractional Share Investing

As described above in this article, fractional share investing involves the automatic investing of cash sitting in your account. The fractional share investing means that at all times your cash is allocated to various ETFs.

In the video below, Tony Robbins gives his thoughts on some of the disadvantages of robo-advisors.

A Summary of Betterment vs. Wealthfront

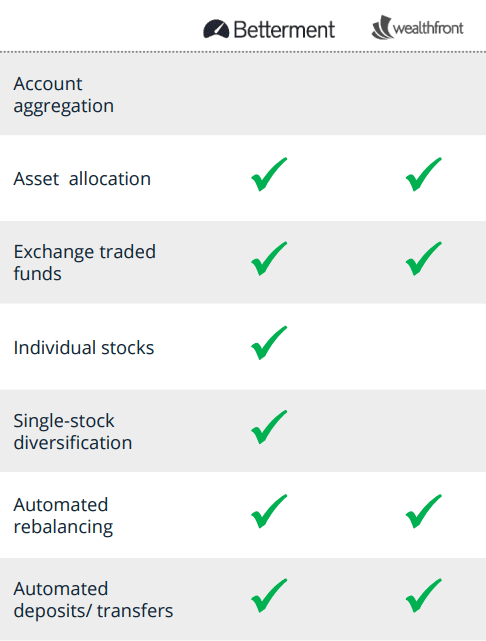

It goes without saying that, these two, offer excellent robo-advisor services. Statistics don’t lie and the respective total assets under management literally tell the whole story. Here is a quick chart to summarize their product and service offerings.

If you are still unsure about whether robo-investing is the way to go, then here is an exceptional unbiased look at the pros and cons of robo-investing.

Blog Post Author Credentials

Louise Gaille is the author of this post. She received her B.A. in Economics from the University of Washington. In addition to being a seasoned writer, Louise has almost a decade of experience in Banking and Finance. If you have any suggestions on how to make this post better, then go here to contact our team.